ATA.Forecast is a generic function for forecasting of the ATA Method.

Usage

ATA.Forecast(

object,

h = NULL,

out.sample = NULL,

ci.level = 95,

negative.forecast = TRUE,

onestep = FALSE,

print.out = TRUE

)Arguments

- object

An

ataobject is required for forecast.- h

Number of periods for forecasting.

- out.sample

A numeric vector or time series of class

tsormstsfor out-sample.- ci.level

Confidence Interval levels for forecasting. Default value is 95.

- negative.forecast

Negative values are allowed for forecasting. Default value is TRUE. If FALSE, all negative values for forecasting are set to 0.

- onestep

Default is FALSE. if TRUE, the dynamic forecast strategy uses a one-step model multiple times (

hforecast horizon) where the prediction for the prior time step is used as an input for making a prediction on the following time step.- print.out

Default is TRUE. If FALSE, forecast summary of ATA Method is not shown.

References

#'Yapar G, Yavuz I, Selamlar HT (2017). “Why and How Does Exponential Smoothing Fail? An In Depth Comparison of ATA-Simple and Simple Exponential Smoothing.” Turkish Journal of Forecasting, 1(1), 30–39.

#'Yapar G, Capar S, Selamlar HT, Yavuz I (2018). “Modified Holt's Linear Trend Method.” Hacettepe University Journal of Mathematics and Statistics, 47(5), 1394–1403.

#'Yapar G (2018). “Modified simple exponential smoothing.” Hacettepe University Journal of Mathematics and Statistics, 47(3), 741–754.

#'Yapar G, Selamlar HT, Capar S, Yavuz I (2019). “ATA method.” Hacettepe Journal of Mathematics and Statistics, 48(6), 1838-1844.

Examples

trainATA <- head(touristTR, 84)

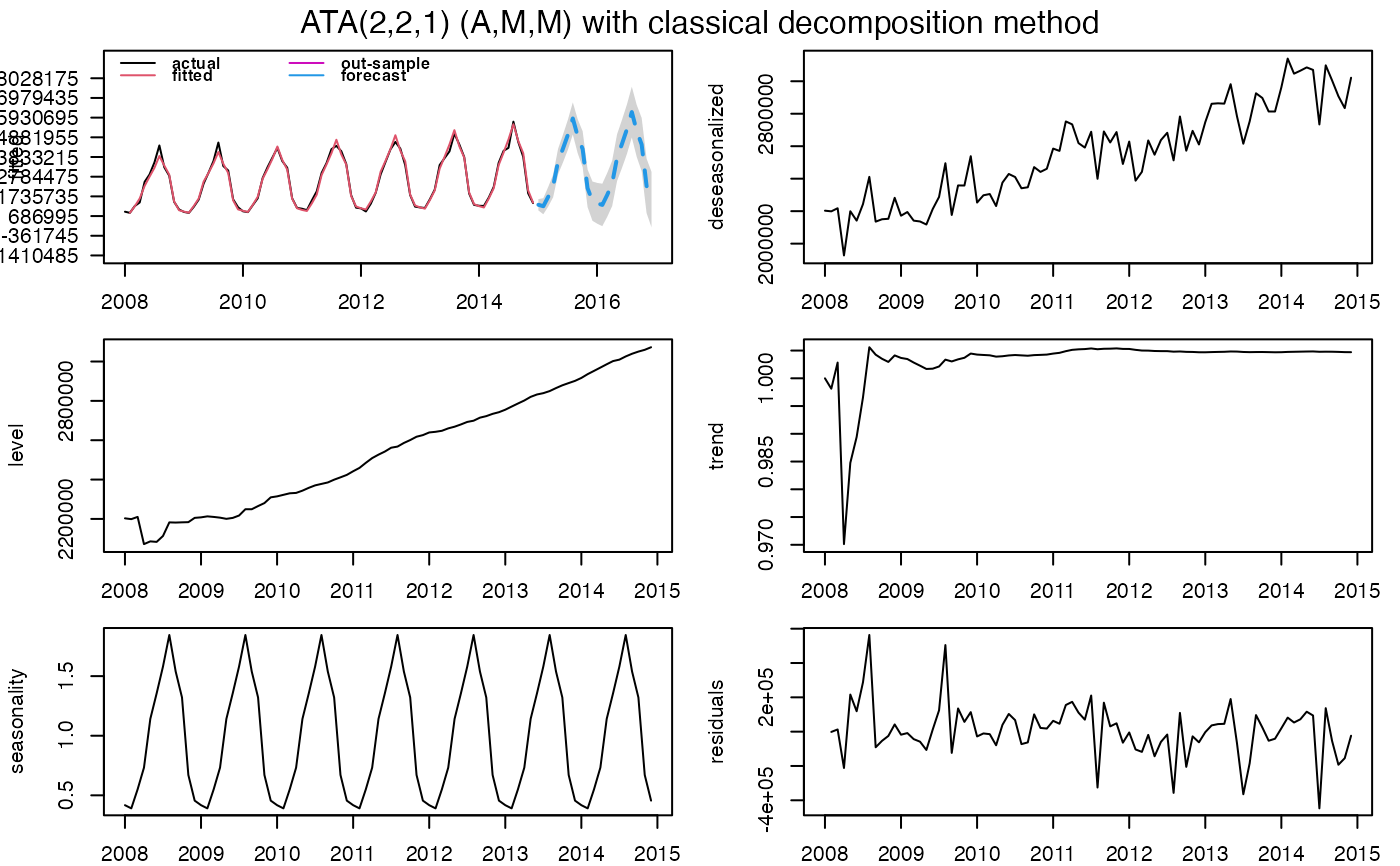

ata_fit <- ATA(trainATA, parPHI = 1, seasonal.test = TRUE, seasonal.model = "decomp")

#> ATA(2,2,1) (A,M,M)

#>

#> model.type: M

#>

#> seasonal.model: decomp

#>

#> seasonal.type: M

#>

#> forecast horizon: 24

#>

#> accuracy.type: sMAPE

#>

#> Model Fitting Measures:

#>

#> sigma2 loglik MAE

#> 25327678645.19519043 -1188.55670094 106527.45549230

#> MSE RMSE MPE

#> 23496762116.62686157 153286.53599265 0.12753452

#> MAPE sMAPE MASE

#> 4.04068178 4.04508846 0.23313082

#> OWA

#> 0.00000468

#>

#> In-Sample Accuracy Measures:

#>

#> MdAE MdSE RMdSE MdPE

#> 67333.7563803 4533834748.2853584 67333.7563803 0.4018348

#> MdAPE sMdAPE

#> 3.2125716 3.2275752

#>

#> Out-Sample Accuracy Measures:

#>

#> MAE MSE RMSE MPE MAPE sMAPE MASE OWA

#> NA NA NA NA NA NA NA NA

#>

#> Out-Sample Accuracy Measures:

#>

#> MdAE MdSE RMdSE MdPE MdAPE sMdAPE

#> NA NA NA NA NA NA

#>

#> Information Criteria:

#>

#> AIC AICc BIC

#> 2391.113 2392.587 2408.129

#>

#>

#> user system elapsed

#> 0.081 0.083 0.313

#>

#> calculation.time: 0.3127

#>

#>

#> Forecasts:

#> Time Series:

#> Start = 2015.00694444444

#> End = 2016.92361111111

#> Frequency = 12

#> [1] 1288568 1211322 1716223 2292963 3589547 4283724 5018661 5887346 4933780

#> [10] 4253560 2170497 1480814 1363260 1281536 1815704 2425875 3797616 4532031

#> [19] 5309568 6228607 5219767 4500118 2296310 1566650

#>

#>

ata_fc <- ATA.Forecast(ata_fit, h=12)

#> Time Series:

#> Start = 2015.00694444444

#> End = 2015.92361111111

#> Frequency = 12

#> lower forecast upper

#> 2015 969867 1271754 1573641

#> 2015 768220 1195153 1622086

#> 2015 1169918 1692802 2215686

#> 2015 1657210 2260985 2864759

#> 2015 2863372 3538412 4213452

#> 2015 3481949 4221419 4960888

#> 2016 4145447 4944165 5742884

#> 2016 4944330 5798196 6652062

#> 2016 3951934 4857595 5763257

#> 2016 3231957 4186608 5141259

#> 2016 1134438 2135685 3136931

#> 2016 410853 1456621 2502389

#> ATA(2,2,1) (A,M,M)

#>

#> model.type: M

#>

#> seasonal.model: decomp

#>

#> seasonal.type: M

#>

#> forecast horizon: 24

#>

#> accuracy.type: sMAPE

#>

#> Model Fitting Measures:

#>

#> sigma2 loglik MAE

#> 25327678645.19519043 -1188.55670094 106527.45549230

#> MSE RMSE MPE

#> 23496762116.62686157 153286.53599265 0.12753452

#> MAPE sMAPE MASE

#> 4.04068178 4.04508846 0.23313082

#> OWA

#> 0.00000468

#>

#> In-Sample Accuracy Measures:

#>

#> MdAE MdSE RMdSE MdPE

#> 67333.7563803 4533834748.2853584 67333.7563803 0.4018348

#> MdAPE sMdAPE

#> 3.2125716 3.2275752

#>

#> Out-Sample Accuracy Measures:

#>

#> MAE MSE RMSE MPE MAPE sMAPE MASE OWA

#> NA NA NA NA NA NA NA NA

#>

#> Out-Sample Accuracy Measures:

#>

#> MdAE MdSE RMdSE MdPE MdAPE sMdAPE

#> NA NA NA NA NA NA

#>

#> Information Criteria:

#>

#> AIC AICc BIC

#> 2391.113 2392.587 2408.129

#>

#>

#> user system elapsed

#> 0.081 0.083 0.313

#>

#> calculation.time: 0.3127

#>

#>

#> Forecasts:

#> Time Series:

#> Start = 2015.00694444444

#> End = 2016.92361111111

#> Frequency = 12

#> [1] 1288568 1211322 1716223 2292963 3589547 4283724 5018661 5887346 4933780

#> [10] 4253560 2170497 1480814 1363260 1281536 1815704 2425875 3797616 4532031

#> [19] 5309568 6228607 5219767 4500118 2296310 1566650

#>

#>

ata_fc <- ATA.Forecast(ata_fit, h=12)

#> Time Series:

#> Start = 2015.00694444444

#> End = 2015.92361111111

#> Frequency = 12

#> lower forecast upper

#> 2015 969867 1271754 1573641

#> 2015 768220 1195153 1622086

#> 2015 1169918 1692802 2215686

#> 2015 1657210 2260985 2864759

#> 2015 2863372 3538412 4213452

#> 2015 3481949 4221419 4960888

#> 2016 4145447 4944165 5742884

#> 2016 4944330 5798196 6652062

#> 2016 3951934 4857595 5763257

#> 2016 3231957 4186608 5141259

#> 2016 1134438 2135685 3136931

#> 2016 410853 1456621 2502389